Two bipartisan House members, Republican Max Miller of Ohio and Democrat Steven Horsford of Nevada, released a discussion draft titled the Digital Asset Protection, Accountability, Regulation, Innovation, Taxation, and Yields Act, or the “Digital Asset PARITY Act.” Despite the name, critics say this bill is anything but fair.

What the PARITY Act Actually Proposes

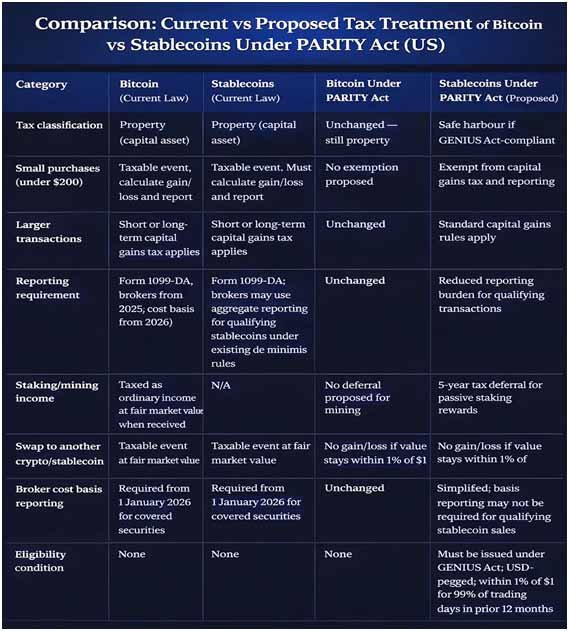

The draft introduces a de minimis exemption for stablecoin transactions under $200, meaning small payments would not trigger capital gains taxes or reporting requirements. It also clarifies that dollar-pegged stablecoins will not incur gains as long as their value remains within 1% of $1.

It’s as simple as it sounds. The Digital Asset PARITY Act protects everyone involved by bringing clarity and parity to the tax treatment of digital assets.

Great conversation with @RepHorsford at @DigitalChamber‘s #DCBlockchain Summit on how we’re working together to bring… pic.twitter.com/dTTrj0fLo8

— Congressman Max Miller (@RepMaxMiller) March 19, 2026

Think of it this way. Spending $5 on a latte using a stablecoin would no longer trigger a taxable event. That is a meaningful change for anyone using crypto in everyday life.

To qualify for the safe harbour, stablecoins must be issued under the GENIUS Act, be pegged solely to the US dollar, and have maintained a price within 1% of $1.00 for at least 95% of trading days in the prior 12 months.

The bill also addresses staking. Staking and mining rewards would receive a five-year tax deferral option, a compromise between current IRS guidance and industry demands. The bill further extends wash sale rules to digital assets and allows mark-to-market accounting for active traders.

So What’s the Problem?

The problem is the name. PARITY implies equal treatment. There is no mention of any tax exemption for Bitcoin, the largest cryptocurrency by market capitalisation. That omission has sparked backlash from Bitcoin advocates who say the proposal creates an uneven playing field.

A person who buys a cup of coffee with Bitcoin still faces a capital gains calculation. A de minimis exemption for everyday Bitcoin transactions is necessary for the digital asset’s maturation as it grows into a global medium of exchange. That was the view of the Bitcoin Policy Institute, which issued a strongly worded response shortly after the draft dropped.

The Bitcoin Policy Institute also faulted the bill’s staking language, which benefits so-called passive validators. The definition structurally excludes Bitcoin miners, who by the nature of proof-of-work, incur high costs for electricity, hardware, and infrastructure.

It creates a two-tier tax regime, offering deferral to stakers while leaving miners facing the same phantom income problem that both parties had already acknowledged needed fixing.

Pierre Rochard, CEO of The Bitcoin Bond Company, put it bluntly. “It’s Bitcoin that should have a de minimis tax exemption. Stablecoins are not decentralised, and they are not permissionless. They’re not real money; they’re just fiat.”

The Coinbase Controversy in the Background

Before this bill even dropped, the Bitcoin community was already on edge. Behind-the-scenes lobbying over the bill attracted controversy when Bitcoin influencers alleged that US crypto exchange Coinbase had lobbied against a de minimis exemption for Bitcoin.

The allegations were denied by several Coinbase executives. The row even drew the attention of X founder turned Bitcoin evangelist Jack Dorsey, who asked Coinbase CEO Brian Armstrong to confirm his colleagues’ denials.

That context makes the bill’s current shape feel, to many Bitcoiners, like a political outcome rather than an oversight.

What Advocates Are Calling For

The Bitcoin Policy Institute has been clear about what it wants changed. Its statement read: “The fix is straightforward. Restore the general de minimis exemption. Extend the deferral election to all block reward recipients, miners and stakers alike, or change the definition to include mining specifically. These changes are the minimum required to deliver on the bill’s own stated purpose.”

Senator Cynthia Lummis has separately put forward legislation that would create a $300 per-transaction exemption, capped at $5,000 annually, while also addressing the taxation of mining and staking. That proposal would cover Bitcoin and other cryptocurrencies more broadly.

The Digital Chamber’s CEO Cody Carbone also took to X to say the industry would keep pushing. “We need de minimis on Bitcoin and will keep advocating that it’s added to this bill.”

Why This Matters for Stablecoin Adoption

Despite the controversy, the bill’s stablecoin provisions would mark a genuine step forward for crypto payments in the United States.

Right now, anyone using USDC or USDT to buy something must track the cost basis of each transaction and report any gain or loss, even if it amounts to cents. That compliance burden is absurd in practice, and it has held back stablecoin use in everyday commerce.

The de minimis rule mirrors foreign currency exemptions and aims to encourage day-to-day crypto payments without triggering complex reporting obligations. The bill also gives the Treasury Department the power to limit the exemption to prevent abuse or tax avoidance.

If this passes, stablecoins would function more like cash in the eyes of the IRS, at least for small purchases. That could accelerate adoption among merchants and consumers who have been sitting on the sidelines due to compliance uncertainty.

Current vs proposed tax treatment for crypto transactions under the Digital Asset PARITY Act.

Is This Bill Going to Pass?

The draft is not yet legislation. As a discussion draft, it is intended to spark debate among lawmakers, regulators, and industry participants before formal introduction to Congress. That leaves room for revisions and mounting pressure.

Representative Miller said last week he believes the broader bill can advance before August 2026. That is an ambitious timeline given election-year politics, but it is not impossible. The bill has bipartisan backing, and crypto tax reform has been years in the making.

The Bitcoin community now has a clear target: get a de minimis exemption added before the bill moves forward. Whether that happens depends on how much pressure lawmakers feel in the weeks ahead.

Also Read: Bitcoin Or Bitcoin ETF: Which Is The Better Investment?

FAQs: US Crypto Tax Bill 2026

Q: What is the Digital Asset PARITY Act?

A: It is a bipartisan discussion draft tax bill introduced by Representatives Max Miller and Steven Horsford that aims to modernise crypto tax treatment in the United States, including a $200 de minimis exemption for stablecoin transactions.

Q: Does the US crypto tax bill apply to Bitcoin?

A: No. The current draft does not include a de minimis exemption for Bitcoin transactions. Bitcoin holders must still calculate and report capital gains on every transaction, including small purchases.

Q: What is a de minimis exemption in crypto?

A: It is a threshold below which small crypto transactions do not trigger capital gains tax or reporting requirements. The proposed bill sets this at $200 for qualifying stablecoins.

Q: When could the PARITY Act become law?

A: Representative Miller has said he hopes Congress can pass a version of the bill before August 2026, though that timeline depends on legislative progress and any amendments.

Q: How does the bill treat staking income?

A: The draft proposes a five-year tax deferral for income earned through passive staking and validation activities, calculated at fair market value when received.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Cryptocurrency investments carry significant risk. Always consult a qualified financial adviser before making investment decisions.

Source:

- https://digitalchamber.org/wp-content/uploads/2026/03/Digital-Asset-PARITY-Act-Discussion-Draft.pdf

- Crypto News

- https://finance.yahoo.com/markets/crypto/articles/bitcoiners-cry-foul-over-us-231742394.html

- https://www.irs.gov/filing/digital-assets