")

Stablecoins Vs Banks: The $500B Wake-Up Call

A fresh warning is coming with a figure that is difficult to disregard.

The Standard Chartered predicts that approximately US500billionmightshiftoutofthedeveloped−marketbankdepositsandmovetostablecoinsbytheendof2028,withstablecoinsscalingtoaUSmarketcapitalisationofUS2 trillion.

It is no longer a niche crypto argument.

That is a commonplace follow-the-money prediction – and it comes to the very heart of the way banks finance themselves.

It also refers to something that ordinary citizens really experience.

Since when does value no longer rest in bank accounts waiting, but instead moves around as tokenised dollars on the rails? Payments do not simply become cheaper.

They become different – faster, always-on, programmable, and simpler to integrate into applications, cards, and business processes.

Standard Chartered says US$500B may move from bank deposits to stablecoins by 2028, making payments instant, always-on, and programmable. (Image Source: AInvest)

Standard Chartered says US$500B may move from bank deposits to stablecoins by 2028, making payments instant, always-on, and programmable. (Image Source: AInvest)

What is the Motivator Behind the Shift Nowadays?

Stablecoins aren’t new.

The new thing is the traction they have gained – and the manner in which large institutions now discuss them as infrastructure.

By January 2026, stablecoins will have a market value many times US$300 billion, and policy and payments players will increasingly view them as a component of money movement to be taken seriously.

And the discussion is no longer whether or not stablecoins will survive.

It is “How fast they rob the banking of the easiest bit of it?

The easiest part is deposits.

Deposits are cheap funding.

Loans The banks put them to write loans, invest and earn a spread.

In case a portion of deposits is washed away into stablecoins, banks do not lose a customer in terms of a customer balance.

They forfeit the low-cost fuel that makes lending margins healthy and more so in the regional banks, which are more heavily dependent on interest income than the giants are.

Why Stablecoins Are Too Good for Payment

The easiest explanation of the attraction would be this.

The transfer of money in the bank is like a business day.

The transfer of stablecoins is like the internet.

It runs on weekends. It clears at night. It is able to clear interbank without a trail of middlemen.

And when a token signifies a dollar, the user does not feel that she or he is purchasing crypto.

They put it as though they are transferring money.

That difference matters.

The write-up on Checkout.com on the payment trends in 2026 even mentions the stablecoins as a better fit for cross-border and B2B flows, in which fees, delays, and trapped capital continue to plague the finance teams.

Things already done by enterprises now overlay.

Treasury groups are time-obsessed. They hate idle capital. They detest settlement windows.

Stablecoins guarantee 24/7 settlement – and that is not a crypto one. It’s an operations promise.

The Ex-Twist in the 2026 Plot: Regulation Makes Maybe a Build

The stablecoins frequently bog down on one huge question: “Is this allowed at scale?”

In the US, 2025-2026 is a move to more transparent structures.

According to the White House fact sheet, the GENIUS Act was signed into law in July 2025, which can be described as a federal approach to payment stablecoins and makes the US a frontrunner in regulated digital dollars.

Simultaneously, legislators continue to advance more stringent regulations of the market-structure.

In January 2026, a Reuters article outlines proposed legislation intended to bring clarity to jurisdiction and establish the rules, and it explicitly refers to the treatment of stablecoins, including the restrictions on the payment of interest to the consumer, just because of the presence of stablecoins.

This is where the spice comes in.

Since the moment regulation has become workable, the stablecoins have ceased to be a side product.

They become a product line.

They become the planning point of banks, card networks, fintechs, and even retail apps.

Banks Aren’t Scared of “Crypto”. They’re Scared of Math

Imagine a sticky deposit base of a regional bank.

Those stores are not just deposits of customers. They constitute the business model of the bank.

Imagine now a world in which a customer will keep less money there, since they can keep it in a wallet of stablecoins that:

- Moves instantly,

- Works globally,

- Plugs into cards,

- Plugs into apps,

- And may even have rewards for activity.

That’s not theoretical.

The leaders of banks are talking more and more about stablecoins as competition for deposits.

The Bank of America CEO stated that the adoption of stablecoins would deplete deposits and increase the cost of borrowing, which was reported by Coindesk.

This is the most overlooked aspect by the non-experts: Borrowing may become costlier when there is a reduction in deposits.

The price does not diffuse out into the air. It collapses on mortgages, business loans and credit.

So yes, this is a crypto story. It is your interest rate story also.

The Money Market is the Place of Battle and Everyone is Selling Shovels

When stablecoins are used as a bigger proportion of money flow, it will not only be the issuers of stablecoins who will win.

The victors will be the rails and interfaces that people already have.

That is why the largest deals in early 2026 are plumbing deals.

This move by Barclays to stake in a stablecoin settlements startup (Ubyx) is an indication that banks are after a clearing layer that is capable of reconciling stablecoins among issuers, rather than a single issuer-single token model.

The same instinct is being demonstrated by the crypto side of the infrastructure companies and Polygon purchasing payments in transactions of more than US250 million: construct a complete payments stack because stablecoins will not scale on dispersed tooling.

This is important to your article on the angle of payments.

Stablecoins are not going to displace Visa or Mastercard in a night. They creep in underneath. They develop into the settlement layer. These turn into the treasury layer. Then, they are the why does my payment clear now? Layer.

The real winners are the rails and apps, not just stablecoin issuers. Deals like Barclays–Ubyx and Polygon’s buys show stablecoins creeping in as the settlement layer. (Image Source: Shoal Research)

The real winners are the rails and apps, not just stablecoin issuers. Deals like Barclays–Ubyx and Polygon’s buys show stablecoins creeping in as the settlement layer. (Image Source: Shoal Research)

The Practical Experience: The Monday Morning Coffee Test

This is a fast method of verifying a payment tech. Enquire whether it is able to withstand the boring stuff.

A tradie paying a supplier. A contractor who is charging a client in a foreign nation. A real estate agent who gathers rent. A small retailer that restocks its inventory following a weekend boom.

Not only exchange trading, but stablecoins are also getting closer and closer to these moments.

In a report on enterprise adoption, Forbes has identified platforms that manage the stablecoin flows to business as an indication of enterprise adoption, citing significant percentage increases in the levels of transactions from 2025 to 2026.

And OMFIF suggests that stablecoins are already at scale in terms of value and movement, which portrays them as more than an instrument in a niche.

Despite being careful with some of the most voluminous claims, their overall direction is similar: Cryptocurrencies cease being an asset and become a utility.

So… Does $500B Actually Move?

The number of $500B of Standard Chartered is based on assumptions.

But the things that are behind it are alive just now:

- Clearer regulation,

- Settlement infrastructure investing institutions,

- Growing enterprise use,

- And the ease of use and convenience of 24/7 digital cash.

The less faith it has in the stablecoins, the more people seek permission to use it like money. They just do.

The sharpness of this forecast is that this structuring of stablecoins is a structural risk, as opposed to a cyclical risk.

Not “crypto is up”. Better said, payment habits develop. And customs are not that readily reversed.

The Implication to 2026 (Not 2028) Payments

Payments teams start experiencing the ripple as early as 2026, before any $500B shift is completed:

- Settlement windows begin to appear optional. When a business is able to settle on-chain at 11:47 pm on a Sunday, the waiting till Tuesday begins to look ridiculous.

- Cross-border is made a product choice, rather than a bank choice. When the tokenised dollars become like a message, cross-border does not feel that much like international banking, but rather that you are choosing the appropriate rails.

- The cards do not disappear; they are given a new backend. The stablecoins may be placed behind card programs and payout systems, and the users continue to tap accordingly. (That is frequently how disruption is really received: unannounced.)

- Rewards will become perverse (and political). Since the lawmakers argue on what stablecoin issuers can provide to holders, the interest vs rewards becomes a red line, particularly when banks claim that they are stable and regulators fear that it is the beginning of shadow banking.

- Banks exert more pressure on their own digital dollars. The issuance-pro-regulating approach allows banks to compete on their own stablecoin offerings, as opposed to the category-wide lobbying only.

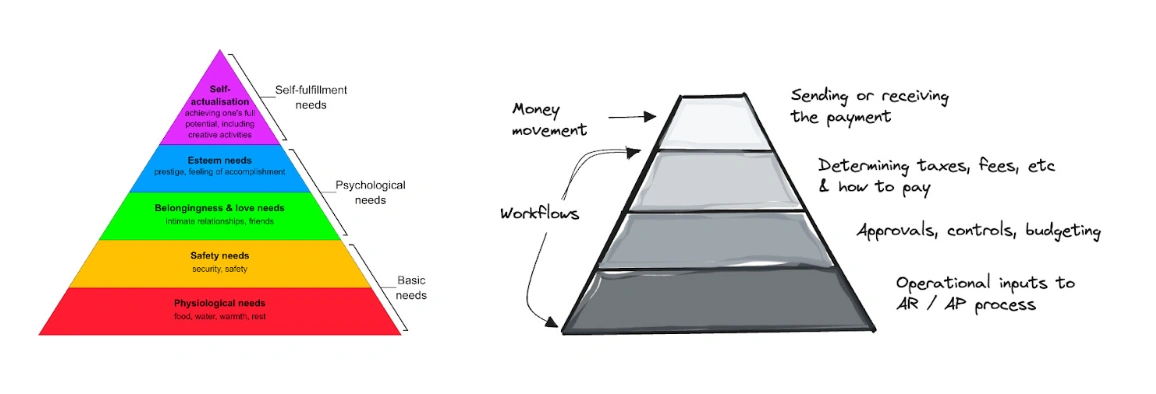

The New Payments Pyramid (Whose Side Really Wins)

Consider payments as a layer cake. The majority of the population perceives the surface, a card tap, a bank application, and a checkout button. Below, there are layers that determine the next step to take. Stablecoins would prefer to reside on the lower levels.

The current stack is in the following form:

- The issuer of the stablecoin (the “ad in the digital cash mint). This is a firm that issues the token and reserves. Simply put, they guarantee the coin would remain valued at around $1. Their sources of revenue are reserved yield and occasionally a partnership. This layer is strong since it is the foundation of the asset. But it is the most regulatory layer as well.

- The blockchain network (the “rail”). This is the place where transfers stand. Here, speed, cost, reliability and network congestion are important. Various networks are competing based on prices, bandwidth, and connections. To users, it’s invisible. It is everything to businesses.

- Containers and wallets (the “container”). Here are the stablecoins in real life. There are wallets which are self-custodial. Other ones are custodial apps that resemble fintech bank accounts. The experience is determined by the container: security, recovery, compliance and user doability.

- On/off-ramps (the “bridge”). This is where the bank money is converted to the stablecoins and vice versa. On-ramps decide friction. They decide on KYC checks. They decide on fees. On-ramps that are smooth will appear to be adopted inevitably. When they are clunky, adoption remains niche.

- Orchestration of payments (the “control room”). Companies do not desire ten different integrations. They desire a single dashboard to pay, receive refunds, reconcile and report. The layer will be the enterprise moat since it integrates into accounting, payroll, procurement, and compliance.

- Merchant acceptance (the “moment of truth”). Here, the stablecoins come in contact with actual expenditure. Online checkouts. Invoicing. Payouts. Subscription billing. In case stablecoins turn into an easy accept of merchants that is non-volatile and a non-accounting nightmare, you experience real scale.

Here’s the key point: The companies that talk the loudest are hardly the winners. Those that possess the dull integration and reporting layer are the winners. That’s where budgets live. That’s where CFO trust lives. That’s where churn dies.

Payments are a pyramid: the tap is just the top. The real winners own the “boring” plumbing; rails, ramps, and integration, where CFO trust and budgets live. (Image Source: Matt Brown’s Notes)

Payments are a pyramid: the tap is just the top. The real winners own the “boring” plumbing; rails, ramps, and integration, where CFO trust and budgets live. (Image Source: Matt Brown’s Notes)

How On-Chain Deposits Actually Work in Practice

Many people listen to deposits moving on-chain and visualize people shutting down their bank accounts and turning into full-time crypto users. That is not the way it most often is. It occurs in the form of small, practicable behaviours and accumulates.

Scenario 1: The “shadow checking account.” The majority of money is stored in a bank where the user is. However, they maintain a stablecoin amount in a wallet of:

- Online purchases,

- Transfers to friends,

- Moving money across borders,

- Refilling a card with international functionality.

It is as though it were a checking account that never sleeps. The bank still exists. But part of the always available balance is lost.

Scenario 2: The business treasury shortcut. A company is selling to it and some of it in stablecoins to operate:

- Supplier immediate payments,

- Faster contractor payouts,

- Weekend settlements,

- Avoiding FX friction.

They may continue doing payroll at banks. However, their working capital begins to work partly off-chain. It is a deposit competition without anybody declaring it.

Scenario 3: The cross-border salary lane. It is at this point that it becomes emotional. An independent worker in Lagos, a project manager in Manila, a web designer in Buenos Aires. They do not desire a five-day international transfer. They don’t want mystery fees. They do not desire a paycheck that will be vetted. With the stablecoins, cross-border payments will become more like messaging. That’s not about ideology. That’s about relief.

Scenario 4: Fix cashflow merchant. A trader takes in stablecoins and remunerates the suppliers using stablecoins. No card chargebacks. Lower network fees. More control. Even assuming that they are reverted to fiat every day, the business initiates a behaviour of looking at stablecoins as a routing alternative. It’s a cash flow tool. Not a crypto bet.

The Largest Misrepresentation: Stablecoins Are Killing Banks

They don’t need to. Banks are capable of remaining giant and yet hurt. Since banks are not simply making money by existing. They earn money due to cheap deposits.

Once the deposits are contestable, all is different:

- Banks interest more to hold money in their hands,

- Margins tighten,

- The money lending is not as generous,

- Compensation comes back in the form of fees.

It ends up being a contest of the silent cash. The wealth that they do not have in mind. This is why this story is significant even to a person who has never touched crypto.

What Banks Will Do In 2026 To Protect The Territory

Banks are not passive. There are three realistic strategies that they possess.

Strategy A: “Fight it.” Lobby hard. Push strict rules. Position stablecoins as dangerous shadow banking. This slows adoption. However, it also runs the risk of driving the innovation abroad or into non-bank players.

Strategy B: “Join it.” Provide tokenised deposits or bank-issued stablecoins. The most natural defensive move is this. It retains customer finances within the banking circle. It also allows banks to provide instant settlement, programmable money and not to lose the relationship. The banks are quick to come to this place, provided there is a regulation to favour it.

Strategy C: “Wrap it.” Banks don’t issue the token. They collaborate with the issuer and are the interface. They will be the end-of-trust and its compliance engine. This is the way the banks remain relevant as they accept that the rails change.

In reality, you see a mix. Big banks experiment. Mid-size banks partner. The reason some of the regional banks fail to do either of these quickly is that they lack the balance sheet or technological budget.

Banks respond in three ways: fight (lobby), join (issue tokenised deposits/stablecoins), or wrap (partner and stay the trusted interface). Big banks test, regionals often struggle.

Banks respond in three ways: fight (lobby), join (issue tokenised deposits/stablecoins), or wrap (partner and stay the trusted interface). Big banks test, regionals often struggle.

Why and Why the Risks That the Experts Continue to Circle Around

When you are going to write to both the experts and the non-professionals, you cannot afford to leave out the tough questions. Stablecoins are powerful. They also carry real risks.

- Reserve quality and transparency. The security of a stablecoin is just as secure as its support. Users want clarity: What assets back it? How liquid are they? What is the frequency of reserves reporting and auditing? It is at this point that regulated structures come in. Not because rules feel nice. Because rules compel standardisation.

- Run risk. In case the users lose confidence, they redeem fast. A bank run is made to appear like a stablecoin run at a higher rate. It’s digital. It’s instant. The system must have guard rails, liquidity planning and clear redemption mechanics.

- Concentration risk: There are a few stablecoins that control the market. Most of the transfers are on a few networks. A few custodians handle large balances. The concentration forms choke points. It is also a source of systemic risk in the case of a failure by one of the major actors.

- Compliance whiplash: Stablecoins are reaching the international movement of money. Those are AML regulations, sanctions, consumer protection, and licensing. When structures are drastically different in various places, then businesses are afraid. The dream that has no friction collides with reality at the compliance layer.

- User experience and security. Self-custody is empowering. It’s also unforgiving. The majority of mass adoption occurs in a custodial or semi-custodial experience. That restores a sense of trust and customer support, but creates counterparty risk. Convenience and safety are currently being struck a balance in the market.

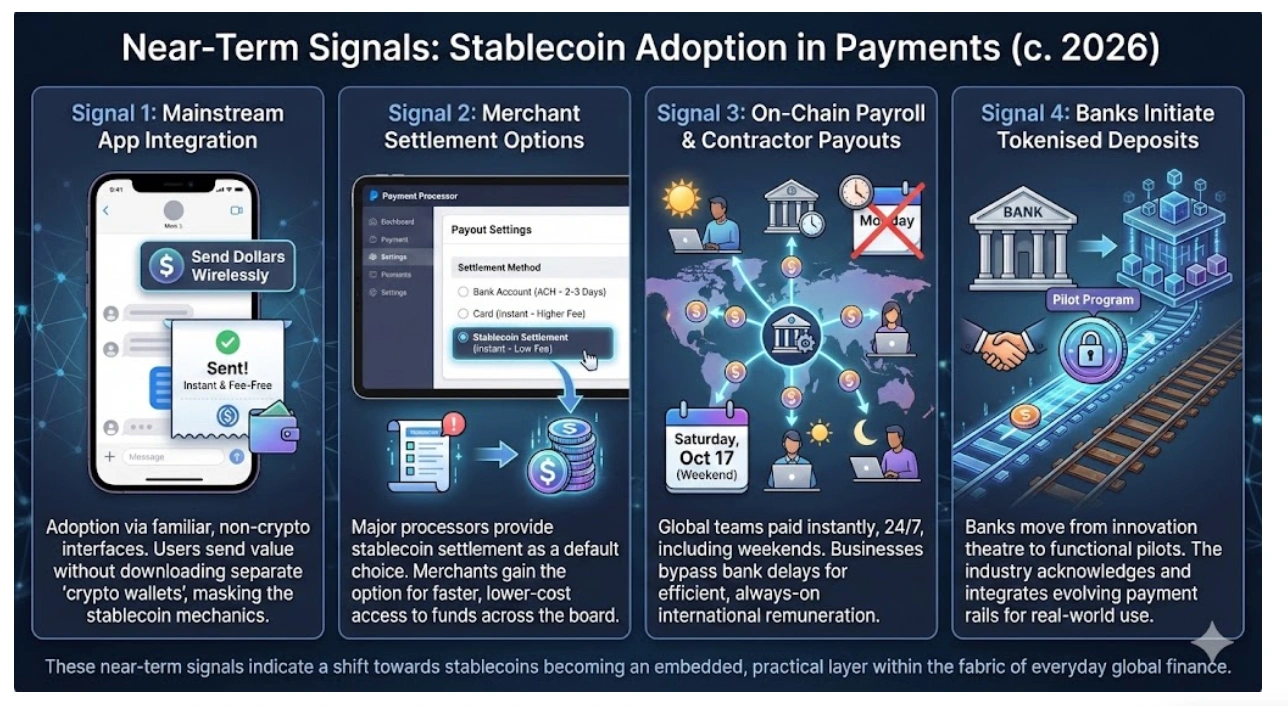

What This Implies About Payments: The Near-Term Matters That Signal

These cues will be in use in 2026, should you wish your article to feel up to date and useful.

Signal 1: Stablecoins are viewed within mainstream applications. Do not download this crypto wallet. More so: “Send dollars wirelessly. Adoption is faster when the stablecoins are not exposed as such through an interface that people are used to.

Signal 2: Merchants begin receiving settlement options in stablecoins. As soon as major payment processors provide stablecoin settlement as a default option, it will be in the game. Not that all merchants use it. The option charges straddle across the board.

Signal 3: Payroll and contractor payouts are transferred on-chain. This is the quiet revolution. Stablecoins would work once business enterprises are able to remunerate international teams during weekends, and the bank will not delay payments. And there are operational tools that are not easily secluded.

Signal 4: Banks initiate tokenised deposits pilots. Once tokenised deposits are made into normal pilots and not innovation theatre, the industry acknowledges that rails evolve. Just like that is the actual inflection point.

2026 signals: stablecoins appear in mainstream apps, merchants get stablecoin settlement, payouts move on-chain, and banks roll out tokenised deposit pilots.

2026 signals: stablecoins appear in mainstream apps, merchants get stablecoin settlement, payouts move on-chain, and banks roll out tokenised deposit pilots.

Real-Life Implications On The Reader

When you are writing to everyday users, provide them with practical tips. Not financial advice. Just pa ractical context.

For consumers:

- Stablecoins act like digital dollars; however, the trust is based on the issuer and platform you are using.

- Custody trade-offs are almost always associated with convenience,

- Regulation is on the move, but disproportionately.

For businesses:

- The cross-border payouts can be reduced by stablecoins.

- Planning requires accounting and reconciliation,

- Conformance installation is more important than the technology.

For banks and fintechs:

- It is not crypto vs the banks,

- It is a 24/7 settlement and money during office hours.

Conclusion

No longer a future of money essay. It is a contemporary contest on what money is doing when it is not being expended. Bank deposits were previously a default. Stablecoins make deposits an option. That is why a 500B change is dramatic. Not due to the number being guaranteed. But that it tells you the direction. And direction, in payment, is destiny.

Frequently Asked Questions (FAQ)

1) What exactly is a stablecoin? A stablecoin is a digital currency that is meant to follow a stable asset, typically the US dollar, so it acts more like cash than a volatile cryptocurrency.

2) Why would individuals transfer bank deposits to stablecoins? Due to the fact that stablecoins can be transferred 24/7 and settle fast, as well as integrate into apps or payment flows, they are particularly useful in cross-border and business transfers.

3) Could the deposits in the claim of $500B be real? It is a prophecy, not an assurance. Standard Chartered connects it with a situation where stablecoins increase to a market capitalization of US 2 trillion at the end of 2028.

4) Which banks are most exposed? Standard Chartered prefers the flag of regional banks as more susceptible as they were dependent on the net interest margin and the deposit funding.

5) Is this increasing the cost of borrowing? It can. When low-cost deposits are lost, banks would increase the cost of funding and with time, that pressure would be transferred into the loan pricing.

6) Do stablecoins primarily serve the crypto traders? That’s changing. The infrastructure deal and expanding transactions into enterprise use of stablecoins indicate a move in the money movement of real-world money.

7) What is the role of regulation at the moment? The accelerant is regulation. Active market-structure initiatives and the GENIUS Act bring stablecoins nearer to mainstream use with specified regulations.

8) Are Visa and Mastercard being ousted by stablecoins? Not immediately. The further development of stablecoins as settlement rails on the bottom of familiar payment experiences is more likely as networks evolve.

9) Are stablecoins currently legal in the US? They work extensively, and regulation changes rapidly. There is a movement of explicit federal regulations and licensing.

10) Are stablecoins interested? That’s contested territory. Policymakers argue about what issuers can provide to the ones holding them and how they compare to bank deposit products.

11) What is the distinction between stablecoins and tokenised deposits? Stablecoins are usually a non-bank (or regulated issuer) and are pegged to reserves. Bank deposits that are tokenised are on-chain deposits, intended to remain within the banking system.

12) Stablecoins: Will they lower payment fees? They are permitted, particularly, cross-border and settlement. However, total cost will be determined by on/off-ramp charges, network charges and provider charges.

13) What industries are adopting payments with the quickest pace with stablecoin? Heavy industries across borders: payroll/contractors, marketplaces, remittances, e-commerce, trading and B2B supply chains across the globe.

14) Can stablecoins be considered long-term safe? Safe relies on the reserve, control, custody and access to redemption. A lot of users consider stablecoins to be a utility balance rather than a long-term store of wealth.

15) Are the stablecoins used to replace SWIFT? Not directly. They are in a position to avoid some of the traditional correspondent banking channels in some of their flows, albeit SWIFT is still central in messaging between banks.