Canada’s Inflation Conundrum: Falling Prices at the Pump, But Pressure Mounts Elsewhere

Just weeks before its next interest rate decision, the Bank of Canada finds itself caught between two competing signals: a headline inflation rate that’s cooling—and a core inflation trend that’s starting to sizzle.

April’s Data Delivers a Mixed Message

On the surface, it looked like good news.

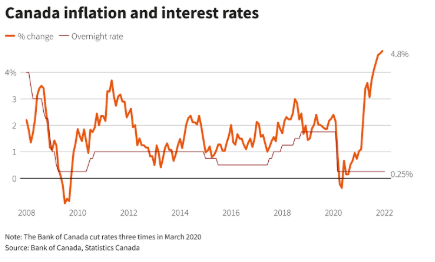

Statistics Canada reported that the annual inflation rate fell to 1.7% in April, down from 2.3% in March. At first glance, it seemed like the Bank of Canada (BoC) was getting the breathing room it needed to cut interest rates in June.

But beneath that encouraging headline figure lies a very different story — one that could derail those hopes altogether.

The Role of Energy in the Decline

Much of April’s Canada inflation relief came from the energy sector. The federal carbon levy was scrapped at the beginning of the month, giving consumers a direct price break at the pump. Combined with lower global oil prices due to oversupply and weakened demand, gasoline prices dropped 18.1% annually, while natural gas prices saw double-digit declines.

In fact, Quebec was the only province where Canada inflation didn’t slow, largely because its own cap-and-trade system kept the carbon pricing intact.

This paints a clear picture: without the energy factor, Canada inflation wouldn’t have cooled so dramatically.

Core Inflation Tells a Hotter Story

When you strip out volatile energy prices, the story changes.

Core inflation, the Bank of Canada’s preferred metric, actually rose to 2.9% in April, up from 2.5% the previous month. That’s a big red flag.

“Unfortunately, the underlying numbers were stronger than most expected,” said Benjamin Reitzes, managing director at BMO Capital Markets. “If the Bank of Canada wants to maintain credibility, it can’t move ahead with rate cuts right now.”

That puts a serious dent in what was, until recently, growing optimism for a June rate cut.

Market Odds: From Confident to Cautious

Only days before the inflation data came out, markets were pricing in a 64% chance of a June rate cut. But following Tuesday’s release, those odds plummeted to under 35%, according to LSEG Data & Analytics.

The BoC had already paused rate moves in April, holding the policy rate at 2.75%, citing the need to assess how trade tensions with the U.S. were affecting Canada’s economy. This new data complicates the situation even further.

A Balancing Act Between Growth and Inflation

The central bank now faces a dilemma: while headline inflation is slowing, signs of underlying price pressures and a weakening labour market are pulling policy in opposite directions.

Canada’s unemployment rate hit 6.9% in April, a sign that the manufacturing sector — sensitive to tariffs and trade disputes — is taking a hit. But higher grocery and travel prices signal that inflation isn’t cooling across the board.

StatCan data showed:

- Grocery prices rose 3.8% in April (vs 3.2% in March)

- Fresh and frozen beef costs jumped 16.2%

- Coffee and tea prices surged 13.4%

- Travel tour prices increased by 3.7% in just one month

For Canadian households, this means that even as they pay less at the pump, they’re paying more at the checkout aisle and while booking vacations.

The Trade War Wildcard

Economists like Andrew Grantham of CIBC say Canada’s economic outlook is being pulled in two directions: inflation remains sticky in core areas, while trade challenges are dragging down employment and productivity.

Grantham suggests that the next GDP report, due shortly before the BoC’s June 4 meeting, could be the deciding factor. “If it shows the economy contracting, a rate cut could still be on the table,” he said.

TD Bank’s Andrew Hencic echoed this, noting that while April’s inflation numbers complicate things, two rate cuts are still possible in 2025 — especially if the tariff-driven slowdown begins to show up more clearly in price data and job numbers.

What’s the Bank of Canada’s Mandate?

At its core, the BoC’s job is to keep annual inflation near 2%, within a target range of 1–3%. It uses interest rate hikes to cool inflation and rate cuts to stimulate growth when the economy slows.

But it’s hard to do both at once. Policymakers can’t simultaneously fight rising prices and support a softening economy — they have to choose what to prioritize.

And with core inflation rising, the pressure is clearly shifting away from immediate stimulus.

The Road Ahead

The coming days are critical. Before its next move, the Bank of Canada will review:

- First-quarter GDP data

- April’s full economic performance

- Signals from global trade partners

- Currency fluctuations and their impact on imports

If data shows deepening cracks in the economy, there may still be a case for cutting rates in June. But if core inflation stays hot, the BoC could be forced to hold — or even warn of future hikes.

Conclusion: Between the Lines

Canada inflation data for April delivered a split-screen reality. One side shows relief at the gas pump. The other reveals price pressures building in everyday essentials — from groceries to travel.

For consumers, it means mixed signals: your commute might be cheaper, but your dinner and vacation just got more expensive. For the Bank of Canada, it means a tightrope walk between supporting growth and preserving credibility in the fight against inflation.

And with only weeks until the next policy announcement, one thing is clear: Canada’s interest rate path is far from settled.

Canada inflation and interest rate