World’s Largest Lithium Mine, WA. Image Credit Alamy

World’s Largest Lithium Mine, WA. Image Credit Alamy

In early 2023, Australia’s lithium juniors were the darlings of the mining sector. Investor capital flowed freely, headlines hyped a battery-powered revolution, and new tenements were pegged almost weekly. Two years later, that optimism is flickering — and for some, fading fast.

Across the ASX and beyond, the question now echoing through boardrooms and outback drilling rigs is blunt: Is the lithium boom already over?

The Price Collapse Few Predicted

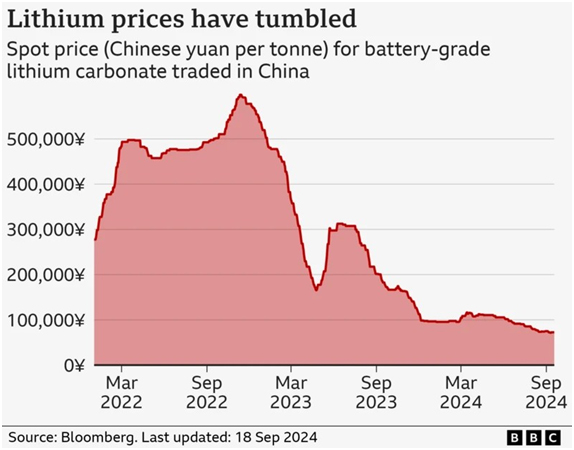

Source: Bloomberg

The lithium price correction that began in late 2024 has accelerated into 2025. Once trading above $80,000 per tonne, battery-grade lithium carbonate has now dropped below $30,000 — a level not seen since early 2021. For large, diversified miners, this is a cyclical dip. But for Australia’s junior lithium explorers, it’s an existential threat.

Most of these companies don’t have production, only drilling results and inferred resources. Their models rely on high prices to attract funding. Now, as investors grow cautious, capital is drying up — and so are drilling programs.

A Wave of Pauses and Cancellations

Several juniors have already announced delays to planned exploration campaigns in WA’s Pilbara and the Northern Territory. Others have quietly shelved feasibility studies, citing “market volatility” and “supply chain concerns.”

In truth, the shift is more profound: many juniors are running out of runway. Those that raised heavily in 2022 and 2023 are burning through cash, while newer entrants are struggling to attract interest in a crowded and cooling market.

Global Supply, Local Consequences

While Australia remains the world’s largest lithium exporter, new supply from Africa and South America has reshaped global forecasts. Chinese downstream buyers, once desperate for secure offtakes, are now negotiating harder or walking away altogether.

This has direct implications for Australian juniors who once relied on Chinese investment to fast-track feasibility or pre-sell production. Without that early capital, many are left exposed.

ASX Reaction: Confidence Cracking

On the Australian Securities Exchange, the lithium index has fallen more than 35% since January. Juniors with no near-term production have been hit hardest. Some, like Core Lithium and Sayona, have publicly reaffirmed their long-term plans — but behind the scenes, cost-cutting and asset sales are quietly underway.

Meanwhile, investors who once flocked to anything with “spodumene” in the title are now diversifying or retreating entirely.

Is This Just the Down Cycle?

There’s no question that lithium demand will rise in the long term. EV adoption is accelerating, battery storage is expanding, and governments across Europe, Asia, and the US are still pushing net-zero targets.

But as one Perth-based analyst put it: “There’s a difference between believing in the future and surviving the present.”

For juniors, the problem isn’t just price — it’s timing. By the time demand rebounds, some of today’s most promising companies may not exist.

Also Read: WA vs QLD: Which State Will Dominate Critical Mineral Exports in 2025?

What Comes Next?

Industry insiders predict a wave of consolidation. Larger miners with cash may scoop up distressed juniors. Others may pivot entirely — from hard rock lithium to rare earths, vanadium, or even hydrogen.

But for now, the mood in Australia’s lithium belt is sober. Drills are quieter. Office floors thinner. And optimism, once a given, is suddenly harder to find.

Final Word

Lithium hasn’t disappeared. Nor has its strategic value. But the hype cycle has burst, and Australia’s junior miners are feeling the full force of gravity.

Whether this is a pause, a pivot, or a prelude to collapse will depend on what comes next — not just in the market, but in how these companies adapt, consolidate, or quietly disappear from the boards they once lit up.